Dataloft Briefing notes address issues raised by our clients as they respond to changing housing market conditions through and beyond Covid-19.

Issue 2: Short term fall in earnings – how vulnerable are UK rental markets?

Short term fall in earnings – how vulnerable are UK rental markets?

Forecasts are notoriously unreliable at the best of times. In the current climate, attempts to forecast economic or housing market indicators come with an almighty caveat. To support our clients in modelling short and long term outlooks in the light of Covid-19, we prefer to set out scenarios for alternative futures.

In this series of Briefing Notes we share our thoughts on aspects of the residential rental market that seem likely to be under pressure as a result of Covid-19 to provide evidence of resilience.

For this paper, we look closely at affordability ratios and model the impact of a scenario under which earnings fall by 20% – a real cirumstance, albeit short term, for many workers in the current climate. Affordability is the metric widely used to gauge renters’ spending power in a market, by showing rent paid as a proportion of earnings.

From our DRMA dataset, we are able to analyse rent paid by an individual renter against their income and calculate the averages from this line-by-line tenancy information. We call this ratio Real Renter Affordability (RRAff) to distinguish it from the conventional measure of affordability which divides average rents in an area by average earnings. We have previously published research which shows that RRAff is considerably less onerous than the conventional measure implies.*

*Real Renter Affordability report, Dataloft 2020

What does the evidence say?

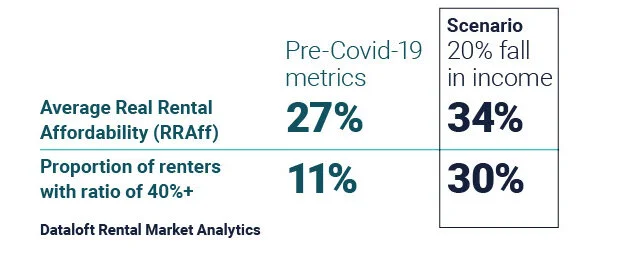

Across the UK, the average Real Renter Affordability, (RRAff) is 27%. In other words, tenants spend, on average, 27% of their gross income on rent. RRAff shows the ratio between a renter’s actual income and the part of rent for which they are personally responsible.

We took a 20% fall in earnings for our scenario on the basis that any tenant furloughed will experience a reduction of at least 20% in their earnings and many businesses have taken that as a benchmark for salary cuts or reduced hours. A 20% drop in earnings, causes the UK average RRAff to shift from 27% to 34% of gross income spent on rent.

London has the highest RRAff – although London earnings are higher than elsewhere in the UK, rents are higher still, by a bigger margin. If earnings were to fall by 20% for London renters, the RRAff ratio would shift from 30% to 38%, making rents considerably more onerous.

Across the UK, around 11% of renters spend more than 40% of their income on rent, using the RRAff metric. If earnings dropped by 20%, the proportion of renters liable for a rent that equates to more than 40% of their earnings would rise to 30% of all renters – a far more significant burden than at present.

Proportion of tenants with a Real Rental Affordability of 40%+ assuming 20% drop in income

% of gross income spent on rent per tenant

UK-wide resilience measures

What does it mean?

Our previous research on RRAff metrics has shown that rental markets are more resilient than is often portrayed. Renters in the private rental sector are very often well-paid professionals earning significantly above the average earnings in a locality. Many share or combine incomes to form a rental household – a factor that conventional metrics struggle to express.

That means that, on average, a drop in earnings of 20% is sustainable, if not desirable. Only in Greater London does a 20% fall in earnings result in a RRAff close to 40%. This is a level that would generally be considered to be problematic and even there, it remains on the right side of the line.

However, in all regions at least a fifth of renters would reach a RRAff of 40% if their earnings dropped by 20%. Therefore, while the market might look resilient, there are individuals that would be pushed into straitened circumstances. Landlords may be well advised to take the initiative with tenants in this situation and avoid the confrontational behaviour that has emerged in the retail sector.

London, inevitably, is more exposed to a fall in earnings because 41% of renters would be pushed above the 40% RRAff threshold by a 20% drop in income. We looked in Briefing Note 1 at the proportion of leases expiring in Q2 and Q3 2020. While London is protected by having later lease expiries, it looks to be significantly more vulnerable to a drop in earnings.

It is worth noting that early indications show that spending is also greatly reduced during this period, meaning there may be more elasticity in RRAff than at other times.

Issue 1: Short term loss of rental income – how vulnerable are UK cities?

Issue 2: Short term fall in earnings – how vulnerable are UK rental markets?

Issue 3: Short term loss of overseas students – how vulnerable are UK rental markets?

Issue 4: Open market rental values – what happened to values in London at the height of lockdown?

Issue 5: Vulnerable employment sectors – which residential rental markets are most exposed to an increase in unemployment?

Issue 6: Single family housing – exploring the opportunity in UK rental markets.

Issue 7: Moving renters – how long do renters stay in their homes?

Issue 8: Community – How important is community to renters?

Issue 9: Eco-Step Scores – Measuring biodiversity in urban areas

Issue 10: Rental potential –Using affordability to assess headroom for rents